A Complete Legal and Cyber Safety Guide to Fake Loan Apps, Digital Lending Scams, and Online Financial Fraud

In today’s digital world, instant loan apps have become extremely popular in India. With just a smartphone and a few documents, people can get loans within minutes. While genuine digital lending platforms have made borrowing easier, the rapid growth of fake loan apps has also created a serious cybercrime problem.

Thousands of people across India have faced:

- Illegal recovery harassment

- Threat calls and blackmail

- Data theft

- Contact-list shaming

- Fake legal notices

- Morphing of photos

- Financial fraud and extortion

Many victims take small loans of ₹5,000–₹20,000 but later face mental harassment, privacy violations, and unlawful demands for huge repayments.

To protect borrowers, the Reserve Bank of India (RBI) has introduced stricter Digital Lending Guidelines in 2025 aimed at transparency, borrower safety, and cyber fraud prevention.

What Is Online Loan App Fraud?

Online loan app fraud occurs when a mobile application or digital platform pretends to provide legitimate loans but instead engages in illegal or unethical practices such as:

- Collecting sensitive personal data

- Charging fake processing fees

- Accessing contacts and gallery without necessity

- Harassing borrowers through calls or messages

- Threatening users with fake legal action

- Misusing private photos or information

- Operating without RBI authorization

These apps often advertise:

- “Instant approval”

- “Loan in 5 minutes”

- “No CIBIL required”

- “Guaranteed loan”

Many operate illegally without proper financial licenses.

Why Fake Loan Apps Are Increasing in India

The rise of digital payments, online banking, and instant credit demand has created opportunities for cybercriminals.

Fraudsters use:

- Fake NBFC partnerships

- Anonymous servers

- WhatsApp marketing

- Manipulated app reviews

- Unregistered lending models

Many apps disappear after collecting user data or money, making recovery difficult.

According to recent reports, digital lending and financial fraud cases have significantly increased in India over the last few years.

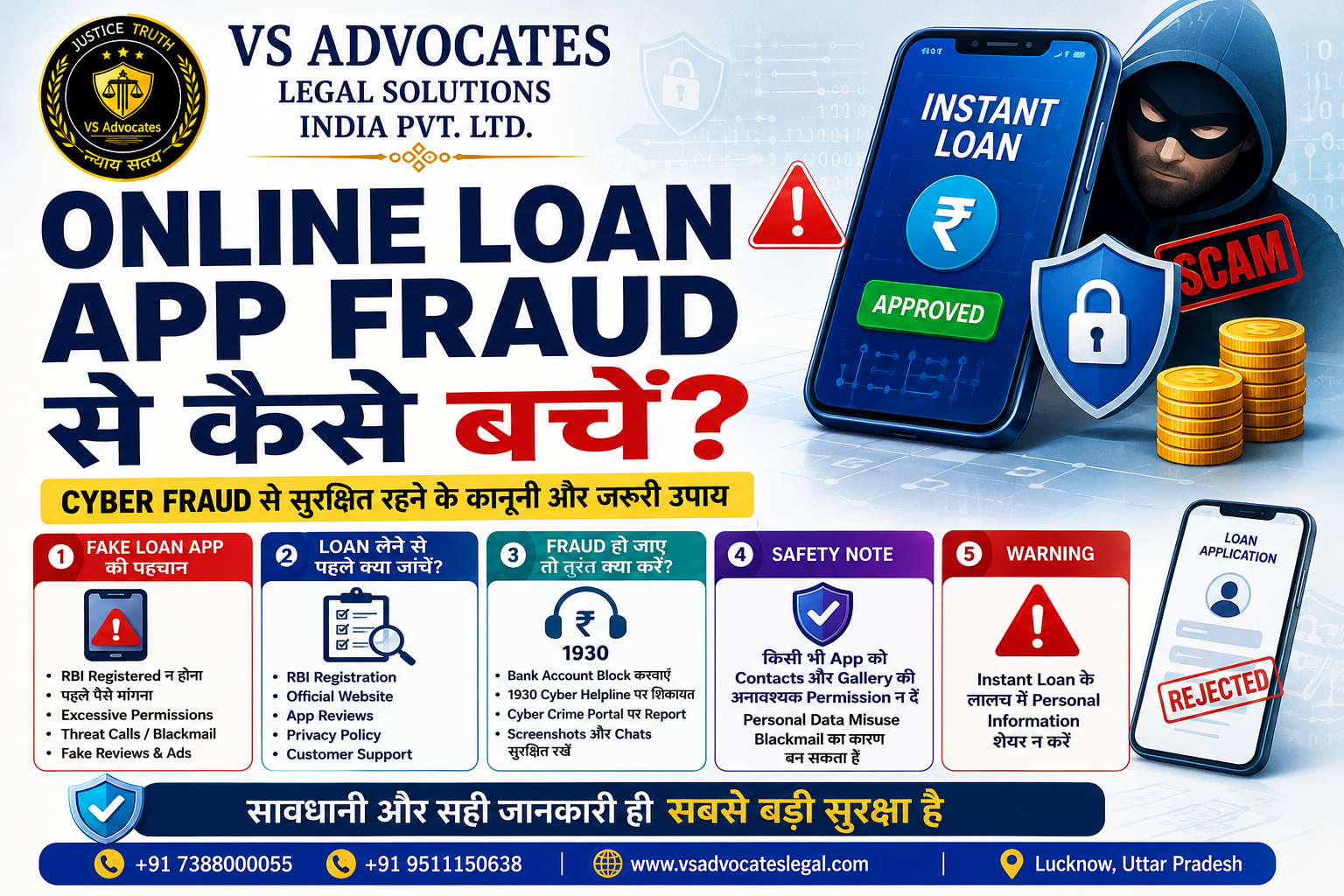

Warning Signs of a Fake Loan App

1. No RBI Registration

The most important check is whether the lender is linked to an RBI-regulated entity.

Legitimate lending in India can only be done by:

- Banks

- Registered NBFCs

- RBI-regulated financial institutions

If the app cannot clearly show its registration details, it may be fraudulent.

2. Asking for Money Before Loan Approval

Fraudulent apps often demand:

- Processing fees

- Security deposits

- Insurance charges

- GST payments in advance

before disbursing any loan.

Legitimate lenders usually deduct charges from the sanctioned amount instead of asking users to transfer money separately through UPI or wallets.

3. Excessive Permissions

Many fake apps ask for unnecessary access to:

- Contacts

- Gallery

- SMS

- Microphone

- Location

- Call logs

This data is later used for:

- Blackmail

- Public shaming

- Threatening family members

- Sending abusive messages to contacts

No genuine lender requires unrestricted access to personal media and contacts.

4. Illegal Interest Rates and Recovery Practices

Some apps provide very short-term loans with:

- Extremely high interest

- Hidden charges

- Daily penalties

- Illegal recovery pressure

Borrowers are often trapped in endless repayment cycles.

The RBI’s latest Digital Lending Directions require lenders to provide complete transparency regarding loan costs, repayment schedules, and borrower consent.

5. Threat Calls and Cyber Harassment

Fraud recovery agents frequently:

- Pretend to be police officers or lawyers

- Threaten arrest

- Send edited or morphed images

- Call relatives and employers

- Abuse borrowers through WhatsApp

These actions are illegal under Indian law.

Cyber intimidation, extortion, identity misuse, and online harassment are punishable offenses.

What to Check Before Taking an Online Loan

Verify RBI Registration

Always confirm:

- Whether the lender is RBI-approved

- The NBFC or bank partner

- Company registration details

- Official business identity

Check the Official Website

A legitimate company should have:

- A proper website

- Registered office address

- Customer support details

- Privacy policy

- Terms and conditions

Avoid apps that only operate through WhatsApp or Telegram.

Read Real User Reviews Carefully

Do not trust only 5-star ratings.

Look for complaints related to:

- Harassment

- Hidden fees

- Blackmail

- Data misuse

- Aggressive recovery practices

Read the Privacy Policy

A privacy policy reveals how your data is handled.

If the app demands broad access to personal information without justification, avoid using it.

RBI Digital Lending Guidelines 2025

The Reserve Bank of India has strengthened regulations to protect borrowers from digital lending abuse.

Key provisions include:

- Mandatory disclosure of all charges

- Borrower consent requirements

- Restrictions on unauthorized data collection

- Transparent lending practices

- Clear grievance redressal systems

- Monitoring of digital lending apps

These rules aim to reduce fraud and improve accountability in the digital lending ecosystem.

What to Do If You Become a Victim

1. Secure Your Bank Account Immediately

- Change banking passwords

- Block cards if necessary

- Disable suspicious UPI access

- Monitor transactions carefully

2. Call the Cyber Fraud Helpline – 1930

India’s national cyber fraud helpline is:

1930

Report the fraud immediately, especially if money has been transferred recently.

Quick reporting improves the chances of blocking fraudulent transactions.

3. File a Complaint on the Cyber Crime Portal

Official Government Portal:

While filing the complaint, preserve:

- Screenshots

- Loan app details

- Payment receipts

- WhatsApp chats

- Threat messages

- Call recordings

These serve as important evidence.

4. File an FIR

If you face:

- Blackmail

- Extortion

- Defamation

- Threats

- Morphed images

- Recovery harassment

you can file an FIR at the nearest police station or cyber cell.

Laws That Protect Victims in India

Information Technology Act, 2000

Applicable in cases involving:

- Data theft

- Hacking

- Identity misuse

- Privacy violations

- Cyber fraud

Bharatiya Nyaya Sanhita (BNS)

Various provisions may apply in cases of:

- Criminal intimidation

- Cheating

- Extortion

- Defamation

- Harassment

RBI Digital Lending Directions

The RBI framework focuses on:

- Fair lending

- Data privacy

- Borrower protection

- Responsible recovery practices

Illegal Recovery Practices You Should Never Tolerate

Recovery agents cannot legally:

- Threaten borrowers

- Abuse family members

- Leak personal data

- Shame borrowers publicly

- Send morphed photos

- Call repeatedly at odd hours

Such conduct may amount to criminal offenses.

Borrowers have the right to dignity, privacy, and lawful treatment.

Why Data Privacy Matters

Your personal data is extremely valuable.

Never share sensitive information carelessly, including:

- Aadhaar copies

- PAN details

- Bank statements

- OTPs

- Selfie verification images

Avoid installing APK files from unknown sources outside official app stores.

Common Loan App Scam Techniques

Fake Processing Fee Scam

The app asks for advance money but never disburses the loan.

Partial Loan Trap

The app credits a smaller amount but demands repayment of a much larger amount with inflated charges.

Contact List Blackmail

Fraudsters message or call friends and relatives to shame the borrower.

APK Installation Fraud

Users are asked to install apps outside the Play Store, increasing malware risks.

Screen Sharing Scam

Victims are tricked into installing remote access apps like AnyDesk, giving fraudsters banking access.

Cyber Safety Tips for Borrowers

- Use only RBI-regulated lenders

- Avoid unknown loan apps

- Never share OTPs

- Limit app permissions

- Read agreements carefully

- Keep screenshots of all transactions

- Report suspicious activity immediately

Should Victims Repay Fraudulent Loan Apps?

This depends on the facts and legality of the transaction.

If the lender:

- Operates illegally

- Uses criminal intimidation

- Violates RBI rules

- Engages in fraud or extortion

the matter may require legal examination.

However, borrowers should never ignore legal notices blindly. Proper legal advice and documentation are essential.

Conclusion

Digital lending has improved financial accessibility, but fake loan apps have also created a dangerous cybercrime ecosystem.

Awareness, caution, and timely legal action are the strongest protections against digital loan fraud.

Always remember:

- Not every instant loan app is genuine

- Not every recovery agent is lawful

- Your personal data must be protected carefully

If you face online loan app harassment, cyber blackmail, or illegal recovery threats, report the matter immediately and seek professional legal assistance.

Important Resources

National Cyber Fraud Helpline

1930

Cyber Crime Reporting Portal

Reserve Bank of India

This article is intended solely for educational and public awareness purposes. For legal action or case-specific advice, consult a qualified advocate or cyber law expert.